Debt Avalanche Method Explained Simply

Feeling stuck with balances and not sure where to start? You’re not alone, and there is a calm, clear way forward.

This guide shows the debt avalanche method in plain terms. The idea is simple: keep minimums on all accounts and put extra money toward the balance with the highest interest rate. When that account is paid, you roll the extra to the next one.

You’ll get beginner-friendly steps, short lists for busy days, and gentle examples for a mom juggling a credit card and a medical bill. We’ll also offer a one-page tracker and tiny daily habits that free up a bit of cash without stress.

This approach can save on interest over time and gives a clear payoff plan so you see steady progress. Together we’ll make a realistic strategy that fits your budget and time.

Key Takeaways

- Put extra money toward the highest interest first to make each dollar work harder.

- Follow short, calm steps that fit a busy life and reduce overwhelm.

- This way often saves more on interest than other payoff strategies.

- Use a one-page tracker and small daily habits to build momentum.

- Real examples show how it works with credit cards and household bills.

Start Here: A calm, simple way to pay off debt faster without overwhelm

You don’t need a perfect plan to begin. Start with five quiet minutes. Gather statements, breathe, and list each balance, interest, due date, and minimum payments—no math yet.

Pick a small, realistic extra amount you can add each month. Even $20–$50 helps. Keep minimum payments on every account and apply your extra to the one with the highest interest first.

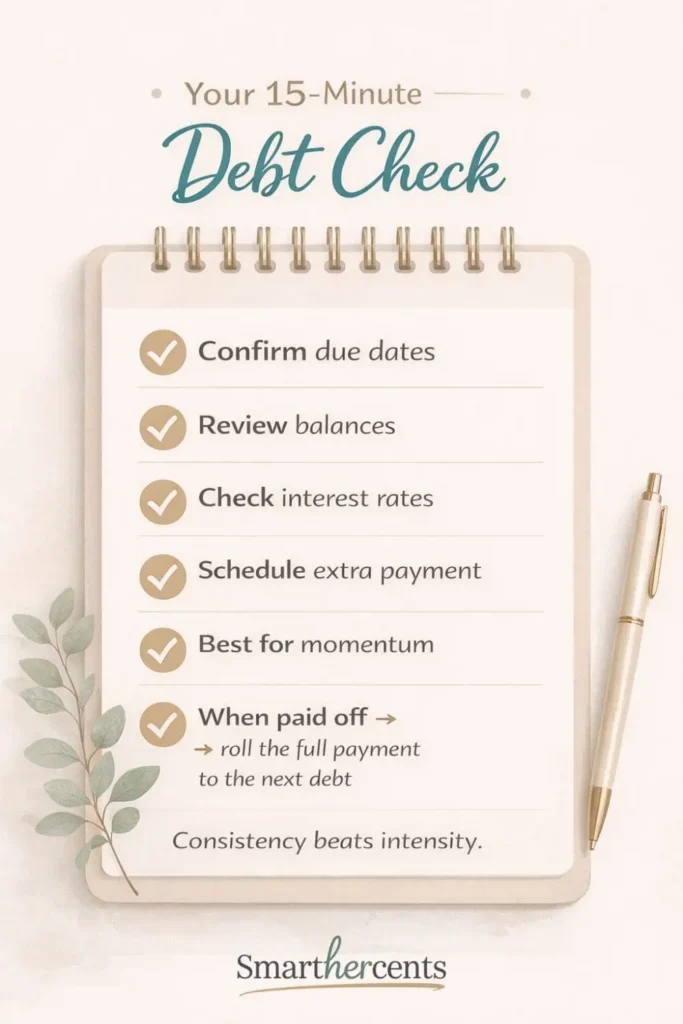

- Weekly 10–15 minute check to confirm due dates and set payments.

- Create a tiny “money corner” — a folder or notes app for your list and logins.

- Soft-start budgeting: essentials first, then see what small amount remains for extra payments.

If numbers feel heavy, set a timer, do one task (like scheduling a payment), and stop. This process is kind to busy schedules. Repeat simple steps, adjust as needed, and let steady actions build your confidence and progress.

Debt Avalanche Method: what it is and why it can save you money

Imagine your extra payment as a tool that trims the most expensive interest first. In plain terms, the debt avalanche method means you pay minimums everywhere and send extra cash to the account with the highest interest rate. When that balance is gone, roll the extra to the next-highest interest.

How it works behind the scenes

APR is the yearly charge on a balance. With compound interest, each month’s interest can be calculated on a growing total. That makes waiting more costly.

Because average credit card APRs sit in the low 20s (22.25% in May 2025), tackling the highest interest first can reduce overall costs and speed repayment.

Avalanche vs. snowball—your feelings matter

- Avalanche: math-first: less interest paid over time.

- Snowball: small-balance wins that help you stay motivated.

Both ways move you forward. Choose the way that makes you feel calm and keeps you consistent.

Step-by-step: use the avalanche method in your real life

Begin by making a simple list you can update in five minutes. Keep it on one page or a single notes app so it’s easy to check.

List your accounts

Write each account with the balance, minimum payments, interest rate, and due date. A short list makes choices clear.

Rank by rate

Put the card or loan with the highest interest rate at the top. If a promotional rate ends, reorder so the debt highest in cost moves up.

Pick an extra amount

Choose an extra amount you can afford each month. Even $20 helps. Keep the number steady and realistic for your budget.

Pay and roll

Make minimums on all accounts, then send the extra payment to the top balance. When that is paid off, roll the full payment to the next item.

Keep it light: set one calendar reminder, automate where possible, and do a short weekly check. This process helps steady repayment without stress.

| Account | Balance | Rate (APR) | Monthly Min |

|---|---|---|---|

| Credit Card A | $2,400 | 22.5% | $60 |

| Personal Loan | $1,800 | 11.0% | $45 |

| Card B (promo) | $900 | 0% (promo) | $25 |

Simple tools and gentle printables to stay organized

A tidy tracker and a few gentle apps help you see steady progress without stress. Small, clear tools save time and keep your plan calm.

Start with a one-page tracker that shows each balance, minimum payment, interest rate, and due date at a glance. This simple list keeps you grounded and reduces mental load.

If you want a simple template

Use a printable one-page tracker that captures each account type, current balance, monthly minimum, and next due date. Add a small column for notes so you can mark promo end dates.

Low-cost apps and spreadsheets

Choose a spreadsheet or an affordable app that auto-ranks by interest rate and lets you reorder items when a promo changes. Look for a view that shows rolling payment so you can see how the next payment grows when one card clears.

- Payoff checklist to remind you when to roll your payment.

- Color-coding for progress—green for paid, yellow for active.

- Keep your budget next to your tracker so extra payment amounts stay clear.

- One weekly reminder and one monthly check to mark progress.

Pick tools that fit your life—mobile, desktop, or printable. The right setup keeps you calm and helps this strategy feel simple and doable.

Everyday habits, frugal swaps, and quick wins that free up extra payment money

Small daily actions can free up a steady stream of extra funds for your payoff plan. These tiny moves are calm, doable, and kind to busy lives. They help you save money and speed paying debt without big sacrifice.

A 5-minute daily money routine to reduce stress and stay on track

Try a five-minute check each day: open your banking app, confirm upcoming payment dates, and move a small amount to your extra payment fund.

Do this in the morning or after dinner so it fits your time and mood. Consistency builds momentum and reduces worry.

Frugal swaps that don’t hurt: groceries, subscriptions, and kid-friendly savings

Pick two painless swaps this month—plan one low-cost dinner weekly and pause a subscription you rarely use.

Choose kid-friendly options like library storytime instead of paid outings, store-brand snacks, and a small weekly grocery cap. Funnel those savings to your highest-rate balance.

Realistic side hustle ideas for busy schedules (weeknights or naptime)

List outgrown kids’ clothes on resale apps, take one evening Instacart shift, or pet sit for neighbors. These tiny efforts can add a helpful amount each month.

Tip: Funnel every little extra to your avalanche method payment. Micro-moves add up and speed your payoff while keeping life gentle and manageable.

Relatable examples: how the avalanche can work on real budgets

Let’s walk through two short stories that show how this plan fits a busy week.

Busy mom snapshot

You have two credit cards and a $1,500 medical bill at 0%.

You make minimums on every account and put extra cash toward the card with the highest interest. When that card clears, you roll the full payment to the next card. The medical bill stays last because its rate is zero.

One 15-minute Sunday session is all she needs to schedule payments and check due dates. Small, steady moves keep things gentle and doable.

High-APR card vs. personal loan

Picture a high-APR credit card and a lower-rate personal loan. You target extra payments to the card first.

This cuts interest faster and shortens total payoff time. Month by month, the total balance drops and the tracker shows interest saved. That progress keeps you motivated.

| Scenario | Top priority | Typical action |

|---|---|---|

| Mom: 2 cards + 0% medical | Card with highest interest | Minimums on rest; extra to top card |

| Card vs. loan | High-APR card | Extra to card to cut interest quickly |

| Real life flex | Reorder if promo ends | Pay minimums during setbacks, resume next month |

Quick tip: If a promo rate ends, update your list so the account with the highest rate moves to the top. This keeps your plan simple and effective without extra stress.

Pros, cons, and choosing your best-fit strategy

Not every plan fits every person—let’s gently match a strategy to your habits. Below are clear, calm points to help you pick a path that you can stick with.

Why the avalanche method often saves the most

The debt avalanche method targets the balance with the highest interest first. That focus usually lowers total interest and can shorten your payoff time when payments stay steady.

It’s a smart, math-first way to save money interest over the long run. If you love seeing exact interest saved, this way may suit you.

When the snowball approach helps you keep going

The snowball method prioritizes small balances so you get quick wins. Those early victories help many people stay motivated and consistent.

If your highest interest is a large balance and the plan feels slow, try the snowball or a short snowball start, then switch back to avalanche to reduce interest later.

| Strategy | Strength | Best fit |

|---|---|---|

| avalanche method | Saves most interest | If you track interest and stay disciplined |

| debt snowball method | Quick wins, momentum | If small closures keep you motivated |

| Blend | Balance of motivation & savings | Start small, then shift to interest-focused repayment |

- Tip: Consider your personality—do you track interest or celebrate closed accounts?

- Either strategy works; pick the way you can sustain with your time and energy.

- Reassess every few months as interest rates, loans, or life change.

Staying motivated and avoiding common pitfalls

A simple habit of tracking and tiny celebrations can change how you feel about monthly payments. Keep your focus gentle and steady. Small checks and kind words to yourself help more than pressure.

Gentle motivation: track progress, celebrate milestones, reorder when rates change

Use a simple tracker or app to watch balances shrink. Seeing numbers move gives a calm, steady nudge on tough weeks.

Celebrate milestones: every $500 paid or each account closed deserves a small, low-cost treat like a home spa night or a library movie date.

If a promotional APR expires, reorder your list so the account with the highest interest rate moves to the top. Keep your minimum payments current while you adjust.

If payoff takes longer than five years, consider a relief conversation

If your unsecured debts—credit card and personal loan balances—look like they’ll take more than five years to clear, it’s time to seek options. A calm chat with a trusted professional can show consolidation or structured repayment choices.

Keep your plan flexible. If an emergency comes up, pause extras, make minimums, and restart when things steady. Whether you pick snowball or avalanche, your steady rhythm and kind self-talk are what carry you through.

- Schedule one monthly check-in to confirm due dates and track changes.

- Reorder priorities if rates or promos change.

- Ask for help early—professionals can review options that support your wellbeing.

Conclusion

, Wrap up your plan with small, steady actions that save interest and make your budget feel clearer.

You now have a calm, step-by-step way to pay debt faster by aiming extra payments at the highest interest rate first. This approach — the debt avalanche method or the avalanche method — helps cut how much interest you pay and shortens your payoff time.

Keep it light: one short weekly check-in, make minimums on time, and send a steady extra to your top-rate balance. A simple one-page tracker or an app that ranks by rate can show progress.

Choose the strategy that fits your energy. Small, kind actions add up each month. You’ve got this — we’re cheering for every step toward a calmer, clearer financial life.

FAQ

What is the debt avalanche approach in simple terms?

It’s a calm, practical plan where you pay all minimums and put extra money toward the loan or credit card with the highest interest rate first. That way you reduce the most costly interest and save money over time.

How does interest rate ranking work?

List each balance with its APR, then sort so the highest rate is first. If a promotional rate changes, reorder the list. Paying the highest-rate balance cuts total interest paid.

Do I still make minimum payments on other accounts?

Yes. Always pay the minimums on every account, then apply your extra amount to the top-rated balance. This keeps accounts current while you accelerate one payoff.

How do I choose the extra payment amount?

Pick a realistic, steady number your budget can cover each month. Even a small extra amount helps. Track spending and use gentle swaps or a short side hustle to increase it over time.

Is this better than the snowball approach?

The high-rate-first plan typically saves more interest and shortens payoff time. Snowball focuses on quick wins by balance size, which helps some people stay motivated. Choose the path that helps you stick with the plan.

What tools can help me stay organized?

A one-page tracker or simple spreadsheet works well. There are also low-cost apps in the U.S. that auto-rank by interest rate and show payoff timelines. Pick what feels easy and calming to use.

How often should I review and reorder debts?

Check your list monthly or whenever a promo period ends, a rate changes, or you add a balance. Small, regular reviews keep the plan accurate and stress low.

What if I can’t make extra payments right now?

That’s okay. Keep up minimums and focus on small, consistent steps like cutting a subscription or trying a gentle side gig. Even tiny gains add up and keep you moving forward.

How much can I save on interest using this approach?

Savings depend on rates and balances. Generally, prioritizing the highest APR reduces total interest more than random or smallest-first payments. Use a simple payoff calculator to estimate your personal savings.

When should I consider professional help?

If balances keep growing, payments feel impossible, or payoff stretches beyond five years, speak with a trusted credit counselor or financial advisor. They can offer options like consolidation or a tailored repayment plan.